If the driver who hit you has no insurance, your situation is serious, but it is not hopeless. In Michigan, you usually do not start by chasing the at-fault driver for every medical bill. You often begin with your own no-fault benefits, and that single fact changes how these cases work. The problem is that no-fault does not cover everything, uninsured motorist coverage is optional, and a claim can get complicated fast if your injuries are significant or your policy has limits.

Why an uninsured driver does not always leave you without coverage in Michigan

Michigan’s no-fault system is built differently than many other states. If you are injured in a crash in Lansing, East Lansing, Okemos, Haslett, or anywhere else in the state, your first source of benefits is often your own Personal Injury Protection, or PIP, coverage. That means the fact that the other driver broke the law by driving uninsured does not automatically cut off your access to medical and wage-loss benefits.

That is the good news.

The harder part is that no-fault reform changed the amount of PIP medical coverage people carry. Many drivers selected capped medical benefits instead of unlimited coverage. So even though your own policy may step in first, you can still run into real gaps if your treatment lasts months, if surgery is needed, or if you cannot return to work quickly. A crash on Grand River Avenue, I-496 near downtown Lansing, or US-127 by East Lansing can create major costs long before fault is fully sorted out.

After a paragraph like that, the key benefits usually tied to PIP are easier to see in a simple list:

- Medical expenses

- Wage loss benefits

- Replacement services

- Funeral and burial expenses in fatal cases

How Michigan no-fault coverage works after an uninsured motorist crash

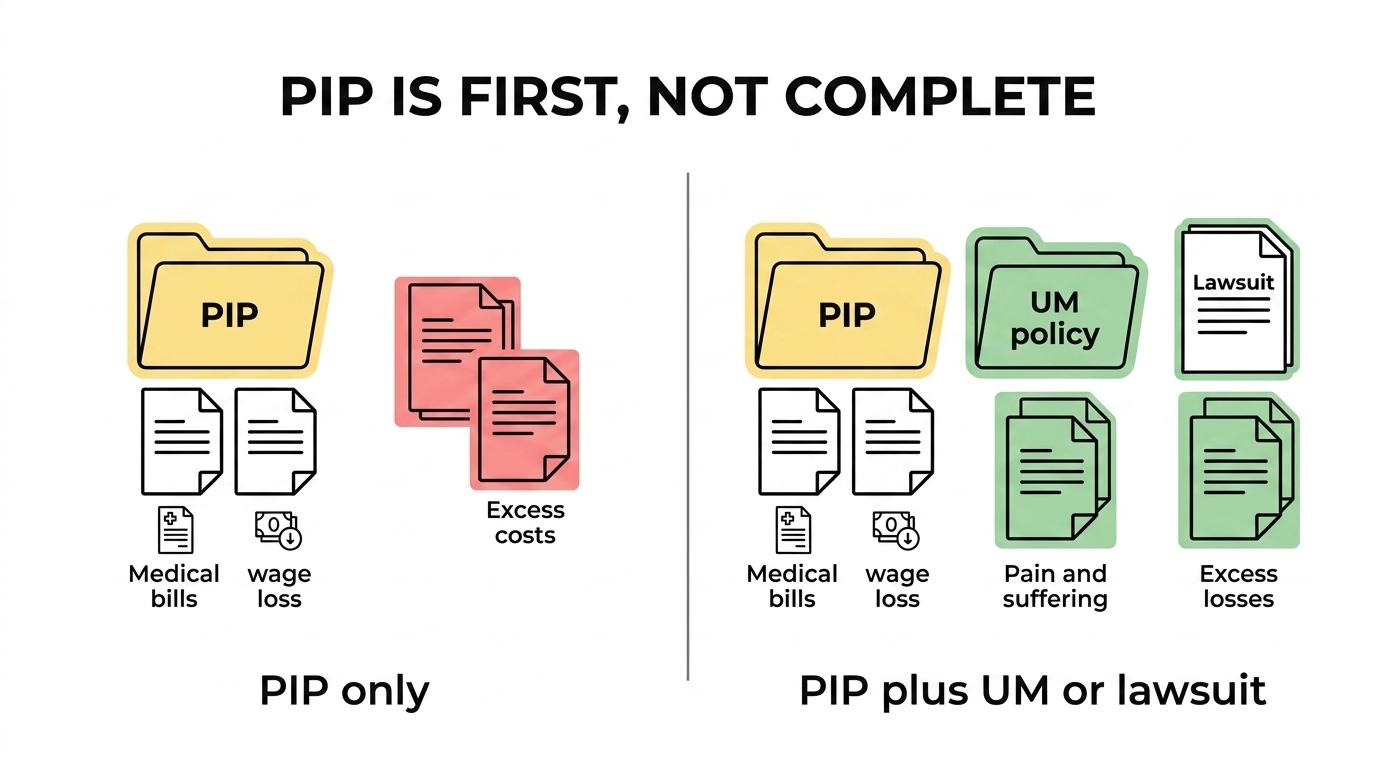

When you are hit by an uninsured driver, your claim usually splits into separate tracks. One track is no-fault benefits. Another may be a lawsuit for pain and suffering or excess losses. A third may involve optional uninsured motorist coverage if you bought it as part of your policy.

Here is the big picture.

| Type of loss |

Typical first source in Michigan |

Main limitation |

| Medical bills |

Your own PIP coverage |

Limited by the PIP level you selected |

| Wage loss |

Your own PIP coverage |

Subject to statutory rules and time limits |

| Pain and suffering |

Lawsuit or UM coverage if available |

You must meet Michigan’s injury threshold or policy terms |

| Excess economic loss |

Lawsuit or UM coverage if applicable |

Must exceed available no-fault coverage |

| No applicable PIP insurer |

Michigan Assigned Claims Plan may apply |

Safety net only, not full recovery in every case |

Michigan currently allows different PIP medical selections, including capped amounts and, in limited situations, opt-out choices. That matters more than many people realize. If your medical care goes beyond your PIP limit, the uninsured driver’s lack of coverage becomes a much bigger problem because there may be no easy pool of insurance money to cover the rest.

You should also know that Michigan law still requires auto owners to maintain no-fault coverage, which includes PIP, property protection, and residual liability coverage. The driver who hit you may have ignored that rule, but your own rights can still depend heavily on whether you had proper coverage in place.

Visualization: The three main paths that can shape recovery after a crash with an uninsured driver.

Where uninsured motorist coverage fits into a Michigan claim

Uninsured motorist coverage, often shortened to UM coverage, is not the same thing as PIP. PIP is part of Michigan’s required no-fault structure. UM coverage is usually optional and based on your insurance contract.

That distinction matters because UM coverage can be one of the most valuable parts of your policy after a serious crash. In many cases, it may help cover damages tied to the uninsured driver that your no-fault benefits do not fully address. Depending on your policy language, that may include pain and suffering damages or losses that go beyond your PIP benefits.

Your policy language controls the details, which is why quick review matters. Some policies have strict notice requirements. Some have arbitration provisions. Some treat hit-and-run claims as uninsured motorist claims only if there is physical contact and timely reporting.

A few points are worth checking right away:

- Policy terms: Look for uninsured motorist or underinsured motorist coverage on your declarations page

- Notice deadlines: Report the crash to your insurer quickly, even if fault seems obvious

- Hit-and-run rules: Some UM claims require fast notice and specific proof

- Coverage limits: Your recovery may be capped by the amount you purchased

When you can sue an uninsured driver in Michigan

Michigan does not let you sue for every car accident loss automatically. Because of the no-fault system, lawsuits are limited to certain categories. If you suffered death, permanent serious disfigurement, or a serious impairment of body function, you may pursue a claim for noneconomic damages, which includes pain and suffering. You may also pursue excess economic loss in some situations if your losses go beyond available no-fault benefits.

That means a crash near the Michigan State Capitol, Spartan Stadium, or the busy retail corridors around Eastwood Towne Center does not become a full civil lawsuit just because the other driver had no insurance. You still have to fit within Michigan’s legal rules.

There is another practical issue that people often overlook. Winning a lawsuit and collecting money are not the same thing. An uninsured driver often lacks assets. So while a lawsuit may be legally valid, the recovery may still be difficult unless there is another source of coverage, including your own UM policy.

The biggest problems you can face after an uninsured motorist accident in Michigan

The hardest uninsured-driver cases usually involve a gap somewhere in the insurance chain. Maybe your PIP coverage is limited. Maybe the other driver has no coverage and no assets. Maybe your own insurer disputes what treatment is necessary. Maybe you were driving a vehicle that was not properly insured, which can trigger serious eligibility problems under Michigan law.

Those issues become even more stressful when you are trying to keep up with treatment, work, and family life. If you work for Michigan State University, a state agency, a local manufacturer, or a major regional employer in the Lansing area, time away from work can create immediate pressure. The same is true if you are a student balancing classes, clinical work, or part-time employment.

The most common trouble spots usually look like this:

- Low PIP limits: Your medical care costs more than the coverage you selected

- Your own uninsured status: Michigan law can bar PIP benefits if you owned an uninsured involved vehicle

- Collection problems: The at-fault driver may not have wages or assets worth pursuing

- Policy disputes: Your insurer may challenge treatment, wage loss, or UM eligibility

- Missed deadlines: PIP and contract-based UM claims both come with strict timing rules

Michigan Assigned Claims Plan and other backstop options

If no applicable PIP insurer can be identified, Michigan has a backstop called the Michigan Assigned Claims Plan, often called the MACP. This can matter in unusual but important situations, including coverage disputes or cases where no identifiable insurer is available to provide PIP benefits.

You should not think of the MACP as a full substitute for solid insurance. It is more limited than a well-structured personal auto policy. Still, it can be an important lifeline when the normal coverage path breaks down.

The point is simple: if your insurance situation is messy, do not assume you are out of options just because the other driver was uninsured.

What to do after an uninsured motorist crash in Lansing, East Lansing, or nearby communities

The hours after the wreck matter. If the collision happened near Frandor, on Lake Lansing Road, around Meridian Mall, or on one of the heavy commuter routes feeding into downtown Lansing and East Lansing, your first steps can shape the entire claim.

You want records, medical proof, and a clear timeline. You also want to avoid casual statements to insurance adjusters that can be used to minimize your injuries later.

A practical response looks like this:

- Get law enforcement to the scene and make sure a crash report is created.

- Take photos of vehicle damage, the roadway, skid marks, weather, and visible injuries.

- Get medical care quickly, whether that is at Sparrow Hospital, McLaren Greater Lansing, urgent care, or through your regular doctor.

- Notify your own insurance carrier promptly and ask for the full policy, including any UM coverage.

- Keep every bill, work note, mileage log, prescription record, and explanation of benefits.

If you were taken from the scene by ambulance, start gathering records as soon as you are able. If you are helping an injured family member, do it for them. Early organization can make a major difference when the insurer starts asking questions.

How Ben Hall Law can help with a Michigan uninsured motorist claim

At Ben Hall Law, personal injury cases are handled with a trial-ready approach. That matters in uninsured motorist claims because these cases often require more than routine paperwork. You may need a careful review of your policy, your PIP rights, the crash investigation, available third-party claims, and whether a lawsuit meets Michigan’s injury threshold.

The firm’s public materials make clear that car accident and personal injury matters include investigating crashes, dealing with insurers, and preparing cases as though they may go to trial. That kind of preparation can be important when an adjuster is minimizing injuries, questioning treatment, or ignoring the full effect the crash has had on your work and daily life.

If you live in East Lansing, Lansing, Okemos, Haslett, or elsewhere in Mid-Michigan, local familiarity also matters. Claims tied to traffic patterns near campus, downtown congestion, student-heavy areas, and major corridors like I-96 and US-127 can involve recurring fact patterns, recurring insurers, and recurring defense arguments. Personal injury cases are also handled on a contingency fee basis, which means attorney fees are not owed unless there is a recovery.

FAQ about uninsured motorist accidents in Michigan

Does Michigan no-fault pay my medical bills if the other driver has no insurance?

Usually, yes. Your own PIP coverage is often the first place your accident-related medical benefits come from, regardless of fault. The amount available depends on the PIP medical level you selected and whether you are eligible under Michigan law.

Can I sue the uninsured driver for pain and suffering?

Yes, but only if your case meets Michigan’s legal threshold. That generally means death, permanent serious disfigurement, or serious impairment of body function. Fault still has to be proven.

What if my medical bills are higher than my PIP coverage?

You may be looking at a combination of health insurance, a lawsuit for excess economic loss, and possibly uninsured motorist coverage if your policy includes it. This is where policy review becomes very important.

Is uninsured motorist coverage required in Michigan?

No. It is usually optional coverage purchased by contract. Many drivers have it, but many do not know whether they bought it until after a crash.

What if I do not know whether I have UM coverage?

Ask your insurer for your declarations page and full policy right away. The declarations page usually lists UM or UIM coverage limits if they were purchased.

Can I still recover anything if there is no applicable PIP insurer?

Possibly. The Michigan Assigned Claims Plan may provide a path to PIP benefits when no applicable insurer can be identified or coverage cannot be determined through the normal process.

What if I was driving without insurance myself?

That can create major problems. Michigan law can bar PIP benefits for an owner or registrant of an uninsured involved vehicle. If that issue is in play, you should get legal advice quickly because the stakes are high.

877-Ben-Hall

877-Ben-Hall